A New Era Beckons

Global GDP at the end of 2019 was at an all-time high, life expectancy rates and financial markets were seeing historical heights, yet these achievements have come at a price. It didn’t take long for the global pandemic to remind markets on the importance of risk management for supply chains, strained community equalities, and the importance of wellness in our priority stack.

Amidst this new awareness, we believe that ‘how’ communities think about the pursuit of happiness will increasingly take into consideration the demand for a more wholistic ecosystem of stakeholders. Meanwhile, the cost of risks to this ecosystem are likely to be repriced, with action coalescing around the major components of the move towards increasing Environmental, Social, and Governance (ESG) functions supporting a shared consciousness toward sustainability.

Many would describe the ESG landscape as a blur in need of clear focus to achieve optimal outcomes for companies and investment groups. Currently, several ranking entities and tools exist to statically assess ESG performance for private and public entities. However, very few data offerings exist to alert asset managers, shareholders, or corporate leadership of risks in real time, or to offer remediation guidance. We see three primary pillars within this effort:

- Recalculating the Cost of Capital: Growing relative incentives for perceived long-term constructive community efforts.

- Rising Regulation: Governments are taking a more active role to allocate cost of assumed long term impact in a linear fashion rather than waiting for system failure before remediation.

- Community Activists Go Corporate: Professional entities are responding to vocal influences (often led by the millennial generation) asserting the values of employees, consumers, local communities and making proactive adjustments to lower perceived risks and/or improve cost of capital.

In this discussion, we will propose strategies and process flow for risk mitigation and increased financial performance to offer a disciplined approach to making sustainability a tangible roadmap. We will also discuss major forces at work within each of the pillars above and identify major contributor groups for global standards and ratings.

MAJOR FORCES AT WORK

PILLAR 1: RECALCULATING THE COST OF CAPITAL

Investors are growing in their embrace ESG factors as an additional component to their overall investment strategy. The impact on a firm’s cost of capital through increased efficiency, relative market share gains, lower operating cost volatility, and lower risk from regulatory penalty is growing in focus, as is the marked increase of inflows into both active and passive strategies to reward these efforts. Clients are voting with their dollars, Wall Street is listening, and the impact on corporate financial performance are just a few of the major drivers leading to an increasingly material recalculation of the cost of capital through as seen through an ESG lens.

Demonstrating this, recent studies have suggested that ESG profiles can already explain as much as a 14% delta in the cost of capital between those viewed as responsible global citizens, and those lacking. As an example, a recent MSCI report, based on data from a study between Dec. 31, 2015, through Nov. 29, 2019, showed that companies’ ESG profiles correlated well with the cost of capital, including both the cost of equity and debt. Specifically, the average cost of capital for the highest-ESG-scored quintile in the MSCI World Index was 6.16%, or 39bps lower than the 6.55% for the lowest- ESG-scored quintile. For the MSCI Emerging Markets Index, the differential was even higher at 103bps. .

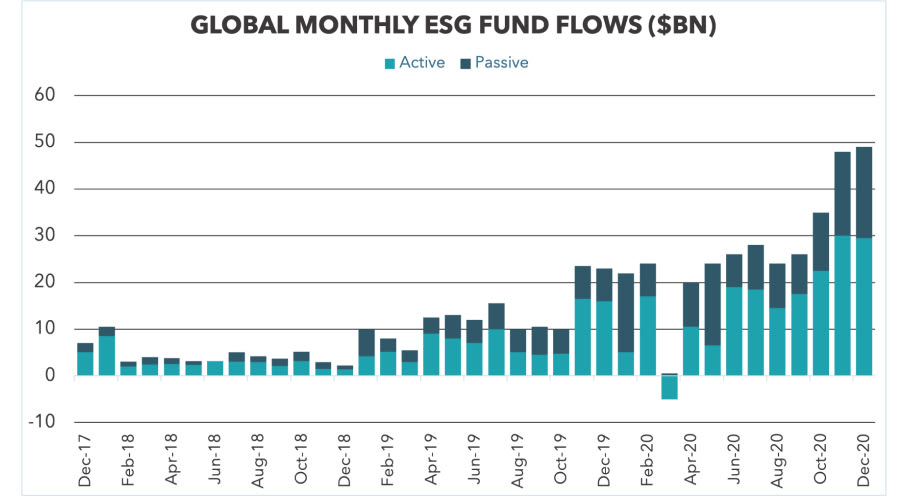

Capital Markets Flows

Further evidence of this accelerating choice to make more capital available to reward perceived good actors can be seen in the record inflows into ESG and other sustainable funds globally and in the US. The commitment to environmental, social, and corporate governance (ESG) has made great strides over the past decade and now has a growing sphere of influence across every industry. More recently, data obtained from Morningstar indicates that October, November, and December 2020 saw record global monthly ESG-related fund inflows of $35bn, $49bn, and $50bn, respectively, bringing total ESG assets under management to almost $1.7 trillion.

ESG-related ETFs and other passive flows represented 30% of the total flows into ESG funds (active + passive), and 21% of the total flows into the broader ETF category. The COVID-19 crisis has accelerated the trend towards ESG investments, with evidence pointing to increased volunteerism, social cohesion, focus on public good, and community support.

ESG & Corporate Financial Performance

Other studies have demonstrated a direct relationship between ESG and Corporate Financial Performance (CFP), validating companies' efforts with sustainable business practices already in place, increasing investor interest, offering further incentive and catalyst for digital initiatives lowering expenses in practical areas such as paper, corresponding storage needs, cost overruns through mismanagement or miscommunication, wasted energy, as well as natural resources such as forestry, food stores, and water. Proactive management of these financially relevant ESG risks align well with management teams, community concerns, and investor interests for less risk and higher return on investment.

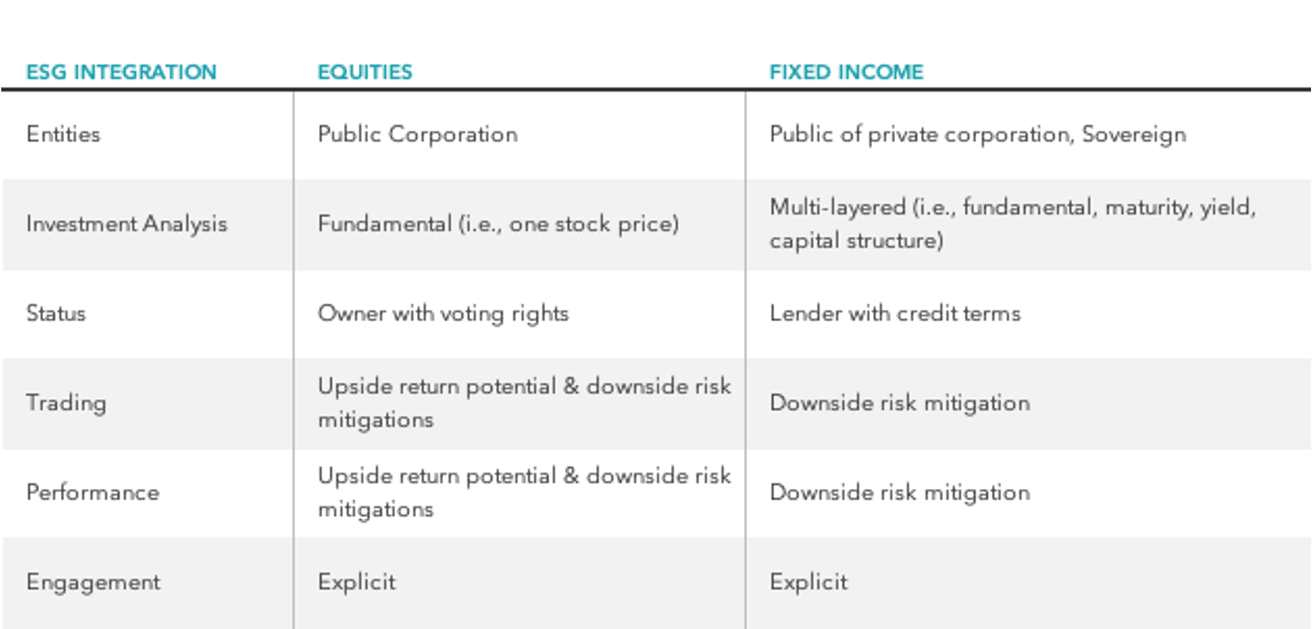

ESG in the Fixed Income and Equity Markets

Historically, fixed income portfolios have been classified by duration and credit quality. ESG provides further clarity into long term sustainability metrics to bring to light issues that can have an impact on risk mitigation and the enduring success of a business. Through this lens, investors can attempt to identify external and company specific factors that may become financially material over time. In fact, given the credit markets are roughly three times the size of equity, with broader reach across public, private and Sovereign interests – this is likely to reinforce the opportunity to broaden the implementation of use cases for ESG evaluation criteria.

PILLAR 2: RISING REGULATIONS

The EU is currently leading on the ESG disclosure front. The Sustainable Finance Disclosure Regulation was introduced in March 2021 and requires mandatory ESG disclosures from asset managers and other financial market players. In December 2020, the US Federal Reserve joined the Network of Central Banks and Supervisors for Greening the Financial System (NGFS), an international group focused on climate change risk, and in March 2021 the SEC formed a task force on climate and ESG to focus on

investment funds marketed as ESG-friendly or ‘green’. As a result, we expect that US banks may soon be asked to assess how risky their investments are to sustainability, while also increasing transparency for investors. Rules are expected to be coming soon for ESG disclosures that will force lending disclosures to incent constructive policies on climate change, among other issues.

The regulatory environment is also seeing changes within the United States. The U.S. Securities and Exchange Commission (SEC) has put plans into action recently announcing that in the area of climate change, it will elevate scrutiny over company evaluation and disclosure of ESG risks. In the crosshairs of the SEC’s newly formed “ESG Task Force“, discrepancies exist in company reports about climate risks under current rules and potential disclosure and compliance issues related to the ESG strategies of advisers and investors. Looking ahead, both the Acting Chair of the SEC and President Biden’s nominee to chair the SEC have forecasted an establishment of a mandatory, comprehensive framework for public company reporting of ESG issues.

Within the next 1-4 years, shareholder voting rights are anticipated to be a focus area with the SEC playing a critical role in the shareholder proposal process. Acting Chair, Allison Herren Lee, has signaled working toward additional goals that include protecting proposals from exclusion if they are related to socially significant issue (such as climate change) just because they may include items that may otherwise be evaluated as ‘ordinary business”. Rules and guidance are anticipated to clearly emphasize the importance of voting as part of funds’ and advisors’ fiduciary obligations to their clients.

The stated priorities of the SEC will also include examination and enforcement with an enhanced focus on climate and ESG (similarly to how cybersecurity and fintech have been incorporated as considerations into the SEC processes due to apparent risk and impact) to ensure alignment with investor’s best interests and expectations as well as assessing firms’ business continuity plans as it relates to relevant risks associated with climate change.

PILLAR 3: COMMUNITY ACTIVISTS GO CORPORATE

A recent survey by Allianz found that a scant 15% of Americans recognize the term “ESG”. Despite low “Brand” recognition, 79% of those same survey respondents liked the idea of investing in a company that cares about the issues ESG represents. While the younger generation is leading the ESG push (64% are more likely to make investment decisions on issues they care about), the older baby-boomer generation lean 42% in support the efforts.

With nothing to lose, who wouldn’t support ESG-friendly companies? In fairness, a survey respondent pays little consequence for their answers. Yet, Millennials have broadly and consistently demonstrated a commitment to act on their views. A majority of the millennial generation believes that companies who care about social issues have better long-term success. It follows then that their lifestyle and investment decisions align with this belief.

This conscious consumer behavior among the millennial generation has influenced the investment world. According to The Deloitte Global Millennial Survey 2020, Millennial values will become more and more important as their purchasing power grows. Emphasizing this growing impact, by the end of 2021, millennials will represent 30% of all retail sales — an estimated $1.4 trillion a year.

ANDURIL OFFERINGS

Although, environmental, social, and governance (ESG) and sustainable investment is a rising focus across the corporate, asset management, and capital allocation communities, we are early into this journey of quantifying many qualitative efforts, and we propose shared frameworks will coalesce across the primary stakeholder pillars. Already, several entities are issuing ranking systems including risk factors, or bond ratings, in specific categories. These entities are becoming increasingly joined by broker dealers and boutique research companies who are seeking to create a more consistent and transparent framework for these metrics. However, very few data solutions/dashboards/KPIs exist to alert asset managers, shareholders or corporate leadership of risks in real time and how these might be ranked across peer groups, or addressed for improvement.

Stakeholder groups who are not sure where to begin are not alone and there are processes and tools available which we believe will highlight the one interest all groups have in common: holistic value creation including top-line growth, cost reduction, regulatory and legal interventions, productivity uplift, and investment and asset optimization.

Anduril Partners offers the following solutions for companies and investors:

ESG MATERIALITY ASSESSMENT AND REMEDIATION

This overall process is essential for companies to understand their organization’s current standing, identify stakeholder groups and audience, set relevant and attainable ESG goals and KPIs, and create a roadmap for achieving them. The outcomes of performing a materiality assessment will create a catalyst for company efforts to then utilize alert-based data analytics to predict changes in future major rating agencies, create feedback loops to recommend and track efforts in progress, and provide reports which can be shared with primary stakeholders.

ESG DASHBOARD AND SCORECARD

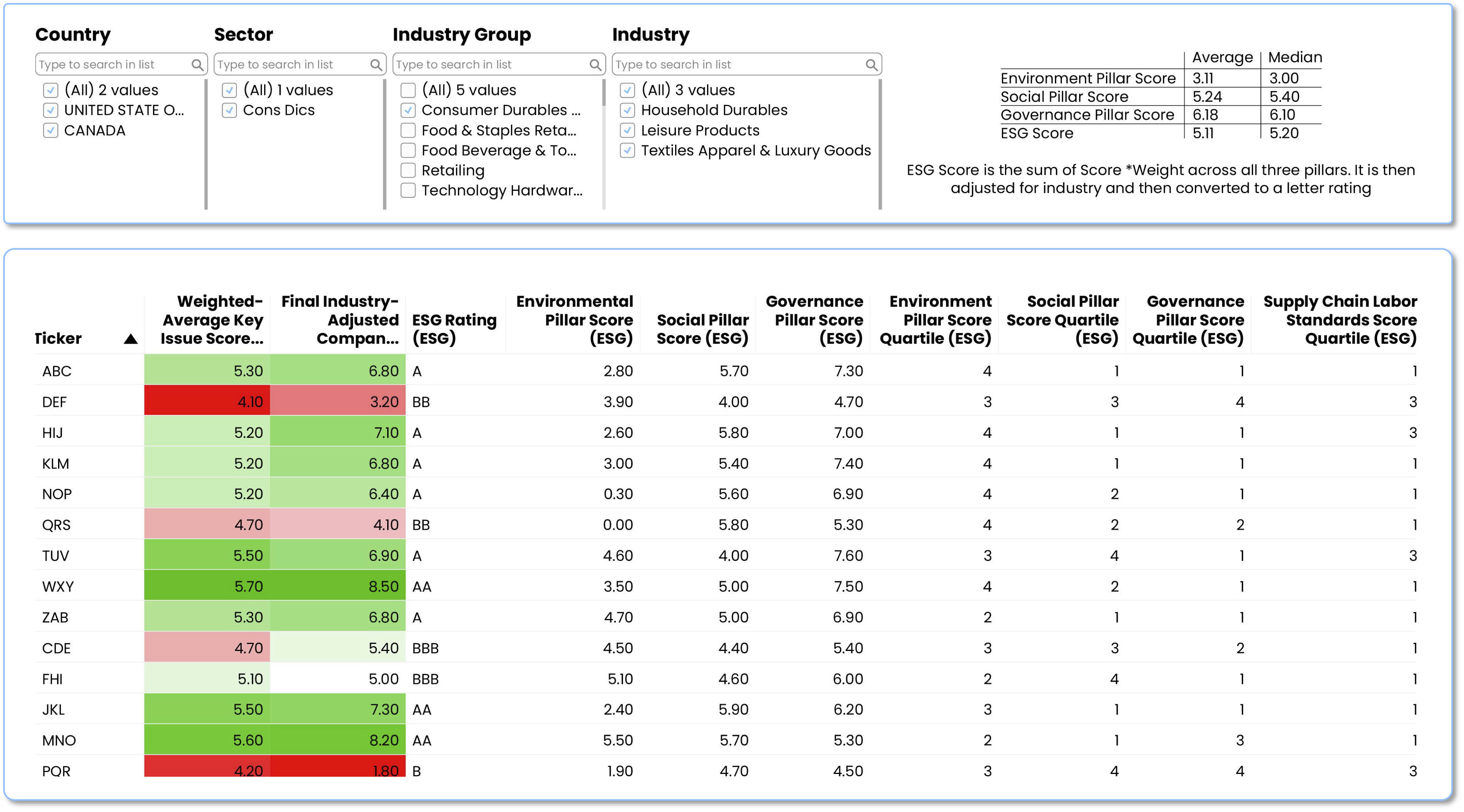

Software solutions will include a customized aggregation platform with dashboards, alerts and a scorecard that allow for granularity in setting specific criteria for an organization to use to achieve individual scores within each category of ESG. Shareholders and corporates can aggregate these views and see relative peer group rankings.

Many asset managers have developed scorecards similar to Table 1. Sample ESG Scorecard (below) that integrate multiple sources of inputs onto a single platform and, further consolidate raw inputs into one or two KPI’s that consolidate inputs through a manageable set of scores that reflect their preferred view.

This methodology provides a consistent, scalable, real time, and transparent process to stakeholders. Corporations and large foundation allocators can also use this with ownership data to see what the ESG scores are for each aggregated investment fund to determine which institutions are really putting their money where their claimed priorities are.

The creation and application of dashboards and feedback loops allow for corporate management to have immediate awareness to mitigate evolving risk. This also allows shareholders and asset managers to be in communication with corporates to determine appropriate and immediate action to respond to alerts.

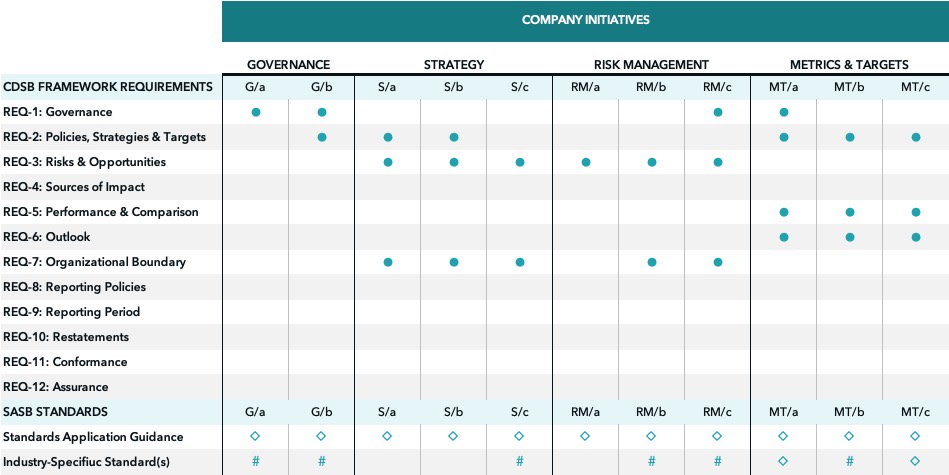

Companies often begin their ESG journey with a simple tracking dashboard that overlays company initiatives over regulatory guidelines. This tool serves to coordinate initiatives company-wide and provides transparency to guidelines not currently addressed. Table 2. Sample Corporate ESG Tracking Matrix (below), provides an example of a dashboard used to identify and track company ESG initiatives. The rows and columns align with the CDSB reporting framework, which is based on CRFD disclosure principles.

ESG PROCESS DEVELOPMENT, IMPLEMENTATION AND IMPROVEMENT

Anduril uses a process framework that is founded on the three pillars introduced in this document (capital, government regulation, and community stakeholders). It leverages industry best practices for decision-making and continual learning and ideally-suited to transform qualitative data into measurable KPI’s and actionable workflows that equip key decision-makers within company ESG programs.

In summary, we believe the three pillars of capital, government regulation, and community stakeholders have similar interests and have the opportunity to reinforce shared goals. Anduril appreciates the acknowledgement of the world that is, and the one we would like to help build including these categories, and currently have early reference accounts working to implement this.

MAJOR CONTRIBUTOR GROUPS

DATA PROVIDERS

ESG data (also termed as non-financial data) has become big business with the demand growing exponentially. MSCI, Sustainalytics, RepRisk, FactSet, and Refinitiv are some of the leading ESG research companies and rating providers who are competing in the market to supply the data. Detailed description of ESG Rating Providers in the Appendix.

GLOBAL REPORTING AGENCIES

Five global reporting agencies; CDP (formerly the Carbon Disclosure Project), the Climate Disclosure Standards Board (CDSB), the Global Reporting Initiative (GRI), the International Integrated Reporting Council (IIRC)and the Sustainability Accounting Standards Board (SASB), are working together to illustrate how their current frameworks, standards and platforms, along with the elements set out by the Task Force on Climate-related Financial Disclosures (TCFD), can be used together to provide a running start for development of global standards that enable disclosure of how sustainability matters create or erode enterprise value. Detailed description of ESG Global Reporting Agencies in the Appendix.

READY TO GET STARTED?

Anduril Partners is eager to help shareholders, corporates and businesses establish, monitor, and communicate ESG data to attract and retain capital, accelerate sustainable and responsible growth, and mitigate enterprise risk. We welcome a conversation. Don’t hesitate to reach out

Jonathan Neitzell

Founder / Managing Partner

Bethany Schuttinga, PhD

Partner / Sustainability Team Lead

bethany.schuttinga@andurilpartners.ai

APPENDIX

ESG RATING PROVIDERS:

- MSCI: Launched in 2010, MSCI ESG Research is one of the largest independent providers of ESG ratings. As part of the MSCI Group, MSCI provides ESG ratings for 6000+global companies and 400,000+ equity and fixed-income securities. Rating: AAA (highest) to CCC (lowest).

- Sustainalytics: The 2008 consolidation of DSR (Netherlands), Scores (Germany) and AIS (Spain). Sustainalytics now covers 7000+ Companies across 42 sectors and has an international presence. In July 2017, Morningstar acquired a 40% ownership stake in Sustainalytics. Rating: 100 (highest) to 0 (lowest) using sector and industry-based comparisons.

- RepRisk: Founded in 1998, RepRisk provides ESG reports for 84,000+ private and public companies in 34 sectors globally. Rating: AAA (highest) to D (lowest).

- FactSet: In October 2020, Truvalue Labs was acquired by FactSet and is now fully integrated into the FactSet platform as a premium service to expand investors’ access to meaningful ESG signals. Truvalue Labs applies artificial intelligence-driven technology to more than 20,000 public and private companies to generate ESG scores on positive and negative ESG behaviors. Truvalue Labs data is mapped to Sustainability Accounting Standards Board standards and United Nations Sustainable Development Goals, allowing investors to evaluate ESG risk factors. FactSet also partners with a number of leading ESG data providers on their Open:FactSet Marketplace.

- Refinitiv: ESG company scores are designed to transparently and objectively measure a company’s relative ESG performance, commitment and effectiveness across 10 main themes, based on publicly available and auditable data. The scores are derived from Refinitiv’s database of 450+ company-level ESG measures, of which a subset of 186 of the most comparable and material data points power the overall company assessment and scoring process. Rating: The score ranges from 0 to 100, with a higher score indicating a stronger performance both on ESG-related disclosures and an absence of events that Refinitiv assesses as being negative for the company concerned.

ESG GLOBAL REPORTING AGENCIES:

- CDP (formerly the Carbon Disclosure Project). A global non-profit that drives companies and governments to reduce their greenhouse gas emissions, safeguard water resources and protect forests. Voted number one climate research provider by investors and working with institutional investors with assets of over US$106 trillion, they leverage investor and buyer power to motivate companies to disclose and manage their environmental impacts. Over 9,600 companies with over 50% of global market capitalization disclosed environmental data through CDP in 2020. This is in addition to the hundreds of cities, states and regions who disclosed, making CDP’s platform one of the richest sources of information globally on how companies and governments are driving environmental change.

- Climate Disclosure Standards Board (CDSB). Founded in 2007 and is an international consortium of business and environmental NGOs committed to advancing and aligning the global mainstream corporate reporting model to equate natural capital with financial capital. It does so by offering companies a framework for reporting environmental and climate information with the same rigor as financial information. In turn, this helps them to provide investors with decision-useful environmental and climate information via the mainstream corporate report, enhancing the efficient allocation of capital. Regulators also benefit from compliance-ready materials. Collectively, we aim to contribute to more sustainable economic, social, and environmental system. CDSB also hosts the TCFD Knowledge Hub on behalf of the Task Force on Climate-related Financial Disclosures.

- Global Reporting Initiative (GRI). The independent international organization that helps businesses, governments and other organizations understand and communicate their impacts. The GRI Standards are the world’s most widely used for sustainability reporting.

- International Integrated Reporting Council (IIRC). A global coalition of regulators, investors, companies, standard setters, the accounting profession, academia and NGOs. The coalition promotes communication about value creation as the next step in the evolution of corporate reporting. The IIRC’s vision is a world in which capital allocation and corporate behavior are aligned to the wider goals of financial stability and sustainable development through the cycle of integrated reporting and thinking.

- Sustainability Accountability Standards Board (SASB). An independent nonprofit organization that sets standards to guide the disclosure of financially material sustainability information by companies to their investors. SASB Standards identify the subset of environmental, social, and governance (ESG) issues most relevant to financial performance in each of 77 industries. SASB also provides education and other resources that advance the use and understanding of its Standards.